One question we get frequently is where are real estate prices headed, North or South? Buyers want to know, and sellers want to know.

The perfect answer is nobody knows for sure, and the market will determine the outcome. A lot of forces are in play that will influence the market. The good news is history and data leave clues. Let’s break down what we know and what history suggests could happen.

Post Hurricane Pricing

Last October we wrote an article entitled Past Hurricane Sales Pricing Data. We showed the pricing trends after Hurricane Charley and Hurricane Irma. It’s also important to note the economic conditions at those times back in 2004 and 2017. Our conclusion was that neither hurricane impacted prices. The economy itself was a larger determinant of what happened following the hurricane than the actual event was.

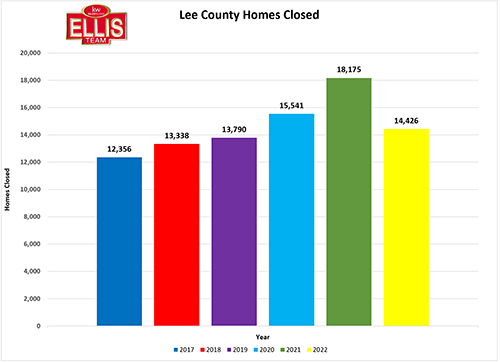

As of this date, closed sales are running almost identical to 2020. In other words, closed home sales are running ahead of 2018, the year after Hurricane Irma. Keep in mind after Hurricane Irma our area was plagued with red tide and blue green algae. While we have had red tide in spurts in 2023, we’ve experienced nothing like we did in 2018. Let’s keep our fingers crossed because 2020 wasn’t a bad year for home sales until Covid squashed home sales in April and May. We rebounded nicely after that, and the rest is history for Florida home sales.

Seasonal Peaks

Traditionally median and average home sale prices peak in April or May, depending on which statistic you look at. We have a few more months left to fully evaluate if we can get back to 2022 levels or surpass them. If we do not, it would not be surprising to see home prices lower year over year the rest of the year. We wrote several articles on that in the past.

One trend we have noticed is pending sales have been tracking interest rates. As rates creep up, pending sales have retreated. As we have received reprieves in rates in certain weeks, pending sales pick right back up. Rates have been down the past few weeks; however, we see them creeping up again.

Interest Rates

Wall street is split on whether the Fed is done raising rates. Some say, including Fed chairman Powell, and some Fed governors, they will raise more. Others say the Fed will have to begin lowering rates as soon as this summer.

If you’re confused, you’re not alone. Wall Street doesn’t know either. If history holds true, we will be watching interest rates. When rates fall below 6%, we could see a resurgence in home buyer activity. If they fall below 5%, we could see prices rise again.

Inventory is Growing

Home inventory has more than doubled in the last year. In fact, our numbers show it tripled. Still, they are low historically speaking, which has helped keep prices up. There would be a lot more listings if sellers were not trapped in their home by low interest rates. So many home sellers would make a move, but they don’t want to give up sub 3% rate on their home.

As the months and years go by, people’s lives change and you will begin to see more homes go on the market. Additionally, when interest rates begin falling, we may see an increase as well. It will be interesting to see how much the demand picks up with falling rates, as well as the supply.

Real Estate Prices Headed North or South?

That mathematical equation will probably determine where home prices go. If you have a home to sell, you should talk to Brett or Sande about our 8-Day Program that nets sellers thousands more than the traditional way. Simply call us 239-444-8150 to get our price on your home.