Average home prices fell 16.4% from May Peak. Last year home prices fell 10.5% in a similar period April through July. Essentially average home prices fell 5.9% more this year than last year around this time.

Home Prices Fell 16.4% From May

I read a lot of headlines that talk about how home sales have fallen but prices are still going up. I would argue that home prices are not going up and whoever wrote the headline doesn’t understand our market.

It is true that median home prices are up 16.7% over last year and average home prices are up 17.4%. That doesn’t tell the whole story. Those are year over year numbers, and they are declining each month because homes are not going up currently. We saw over $100,000 median price gain from September 2021 to April 2022. We saw $188,000 gain in average price from September 2021 to May 2022. Since April/May it’s been downhill. We are still up year over year because most of the gains happened from September on.

The real numbers will begin to show in October once official September numbers are released. From this coming September to April, we will get an excellent idea of how the market is doing. We can already see home prices are down slightly, but to calculate how much of that is from seasonality is hard to do.

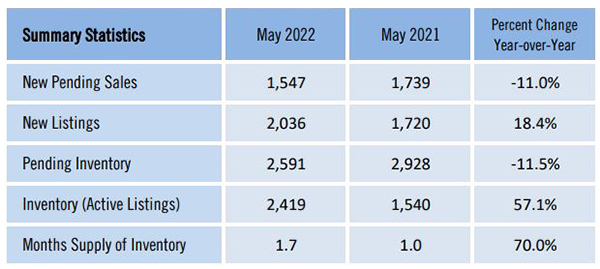

What seems absurd is the fact some people believe home prices are still appreciating. Listing inventory has tripled since February, pending sales are down, and closed sales are down. This is not a sign of an appreciating market. Home buyers know it, and home sellers know it too. I appreciate the media putting a good spin on the market, but quite frankly we don’t need a good spin.

The market is what it is, and always will be. You cannot spin the market into something it is not. When inventory is rising it means supply is outpacing demand. When inventory is falling it means that buyers are scooping up properties faster than they come on the market.

Simple Law

We have an excellent market, if you price your home fairly and market it aggressively. This simple law works in all markets, up, down, or sideways. Hire the best Realtor you can find, market the property for full exposure to the largest number of buyers, and price it fairly. I’ve seen sellers miss the best seller’s market we’ve ever seen, and I’ve seen buyers miss out on the best buyer’s market we’ve ever seen.

Buyers and sellers typically miss the market out of greed. The truth is, over just about any 10-year period real estate is a good investment. Don’t get too greedy and you will never miss the market. Sure, real estate can go down in the short term. In the long term, real estate has done well, and even better than the stock market.

Don’t believe everything you read or hear. Consult a local market expert. While we are experts in this market, we would never purport to be an expert in another market. Listening to someone from another state about how to negotiate or price a home locally doesn’t make sense.

Always go deeper than the headline. Sometimes the headline doesn’t match the content of the story. Ask yourself if the data makes sense and seek out numerous opinions if you are unsure. When you hire the best, you tend to get much better results. This is true in any profession.

Always Call the Ellis Team

If you are thinking about selling your SW Florida property, give the Ellis Team a call. We have the knowledge, experience, and marketing muscle to expose your home to the largest audience. 239-310-6500 Find out if your home is going up or down in value online for free!

Good luck and Happy Selling!